Speculative Bubbles in History

A Perspective on an Unsettled Concept

By William Quinn and John Turner

{kind=link}

Although the “speculative bubble” is one of few financial concepts to regularly show up in popular culture, in academic financial economics it is a remarkably controversial topic. There are unresolved debates surrounding what constitutes a bubble, whether bubbles actually exist, whether central banks should take action in order to ‘prick’ bubbles, and why, exactly, bubbles often lead to economic recessions.

What Is a Bubble, Really?

Even the use of the word “bubble” can provoke the ire of economists: Peter Garber describes it as “a fuzzy word filled with import but lacking any solid operational definition”, whereas Eugene Fama simply states that “the word ‘bubble’ drives me nuts”.

Assuming that bubbles actually exist as a recurring phenomenon, how should they be defined? Charles Kindleberger defined a bubble as any substantial upward price movement followed by a crash. This, however, feels incomplete: if an industry grew due to unforeseeable good news, before shrinking due to unforeseeable bad news, it would not seem accurate to describe the event as a bubble. Peter Garber therefore proposes defining a bubble as “a price movement that is inexplicable based on fundamentals”, which seems more consistent with the popular understanding of the word.

A problem with Garber’s definition is that, although it is more precise, it renders bubbles impossible to identify with certainty. This is because testing for market efficiency always invokes a ‘double hypothesis’ problem: one can never tell whether prices were truly inconsistent with fundamentals, or they just appear to have been because the pricing model used for the test was incomplete.

One solution is to avoid using the word ‘bubble’ at all. But given how frequently the concept appears outside of academia, it would be absurd if academic finance had nothing to say on the subject at all. In practice, the most sensible solution is often to revert to Kindleberger’s definition.

Why Bubbles Matter

Why are economic historians interested in bubbles? There are purely historical reasons to be interested in these events: they have often played a central role in the development of financial markets and corporate law, most notably with the Bubble Act of 1720. However, this is also a field in which the past can directly inform the present.

The potentially severe economic consequences of bubbles makes their study essential, but they are also rare events, and acquiring an overview of the subject is almost impossible without a historical perspective. Economic history has therefore recently contributed to three areas of contemporary, policy-relevant debates surrounding bubbles.

The first area is the central question of whether bubbles represent examples of market irrationality. The historical evidence on this point is somewhat mixed. Qualitative evidence has been used to suggest that bubbles result from mass irrationality, or, as Charles Mackay put it, the ‘madness of crowds’.

Madness or Model Error?

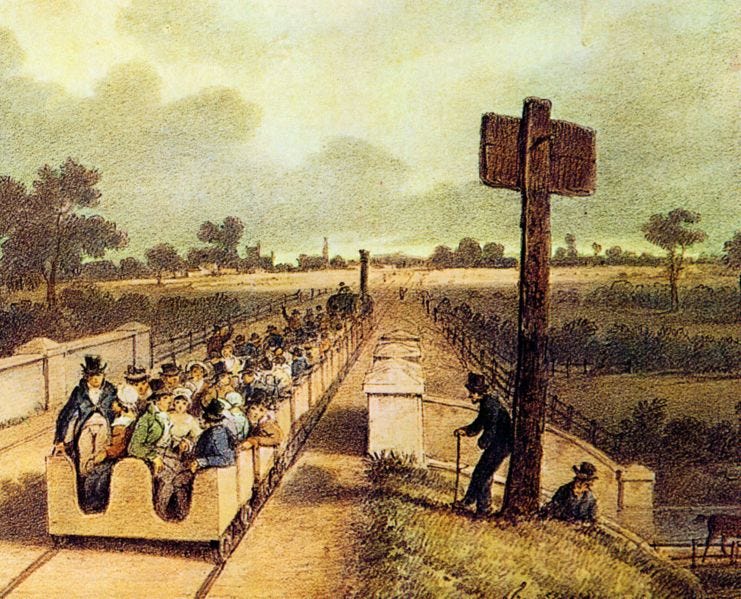

However, closely analyzing share prices during famous episodes often contradicts these stories. That doesn’t mean prices at the peak were “correct,” but in hindsight, they often appear justifiable given the models investors used at the time. For example, Gareth Campbell has shown how prices during the British Railway Mania, although inaccurate in hindsight, were generally consistent with the pricing models widely used at the time. In practice, these models overestimated the sustainability of high initial dividends. But this is a long way from the ‘madness’ described by Mackay.

The evidence from historical bubbles suggest that, while prices might not always have perfectly reflected underlying fundamentals, the popular characterization of bubble investors as naïve fools absorbed by a speculative frenzy is inaccurate.

{kind=link}

To Prick or Not to Prick: Central Banks and the Politics of Prevention

The second area is the question of whether central banks should raise interest rates in order to ‘prick’ a bubble, thereby preventing adverse economic consequences if it is allowed to grow. There are strong economic arguments for and against this point, but historical evidence generally suggests that it is a bad idea. Ben Bernanke, among others, has argued that the attempts of the Federal Reserve to burst the asset price bubble on the eve of the Wall Street Crash were partly responsible for the Great Depression. Hans-Joachim Voth has convincingly shown that a similar mistake was made in Germany in 1927, with even more severe political consequences.

The counter-argument put forward by Nouriel Roubini is that these particular examples involve monetary policy which was ‘botched’, and more well-informed efforts to influence asset prices could be effective. This is theoretically possible, but any historical examples seem insignificant in comparison to the severe consequences of the aforementioned attempts to burst bubbles in the 1920s.

When the Bubble Bursts

The most consequential question may be what comes after a bubble: why do so many end in economic crisis? Here there are two plausible mechanisms: the ‘wealth effect’ and the ‘debt effect’. The wealth effect argument is that the bursting of the bubble inflicts heavy losses on investors, who respond by decreasing spending, thus reducing aggregate demand. The debt effect argument is that, after the bubble bursts, demand is reduced because the public are less inclined to borrow, and banks are less inclined to lend.

A 140-year study by Óscar Jordá, Moritz Schularick, and Alan Taylor finds that, while both of these mechanisms seemingly occur, recessions are much more severe when the bubble was accompanied by a high level of leverage. John Turner in his book Banking in Crisis, has suggested that bubbles which are driven by indebtedness, such as the housing bubble of 2006-07, are particularly dangerous for banking systems and economies.

This article was originally published by The Long Run and is reprinted here with permission of the Economic History Society.